Interest deductibility - a property investment case study

Introduction

The impact of removing interest deductibility from investment properties is only just starting to be seen in the market. Most people are only just grasping the impact it will have on their property investment portfolios. In this blog I’ll give a brief outline of the legislation, and give a real world example of the impact of the changes to the financial feasibility of a rental property.

How does the changes to Interest Deductibility work?

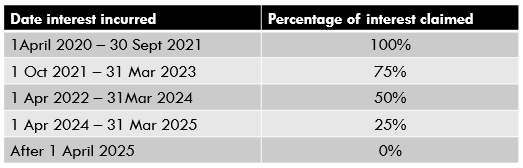

Since 1 October 2021, the following rules apply:

Interest cannot be claimed for residential property acquired on or after 27 March 2021 unless an exclusion or exemption applies.

The ability to deduct interest is being phased out between 1 October 2021 and 31 March 2025 for properties acquired before 27 March 2021.

There are a number of exemptions to these changes including:

New builds

Dealers, builders, and developers

Emergency, transitional, and social housing (e.g. Kainga ora)

Some staff and student accommodation.

Case Study

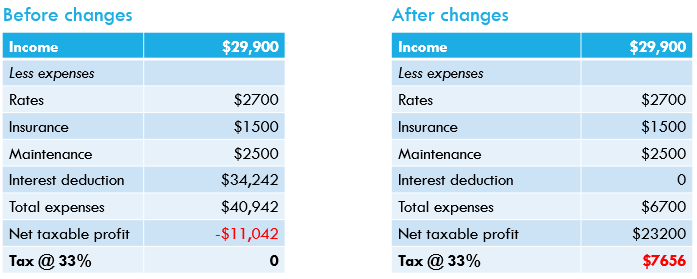

4 bedroom 1 bathroom house, 1 car garage, good suburb in Dunedin. It was rented at $575 per week.

This property was bought in 2020 prior to the changes taking affect. The initial interest rates were very low and the property was breakeven from a cashflow perspective. In early 2023, the fixed interest rate on the property increased substantially making the property a negative cashflow proposition. Below displays the financials of the property a) before tax deductibility, and b) after 100% deductibility gone.

The net result of the changes is that the property which has a negative annual cashflow of approximately $11,000 now also has an annual tax bill of $7700. This means that the property will now cost the owner approximately $19,000 per year to hold the property. If we factor in the 10 year Brightline test for capital gains then it will cost the owner $190,000 to hold the property before they could sell it and hopefully make a profit.

Summary

These changes bring into question the feasibility of investing in residential property where this legislation applies. It could result in investors pulling out of these type of properties and re-allocating their investment capital into other areas including exempt residential properties, commercial property and non property investments. This could be positive for first home buyers but could also increase the shortage of rental properties in Aotearoa.